The Addendum That Decides What Happens When the Appraisal Comes In Low

Most buyers include the appraisal addendum in their offer. Most sellers don’t think about it until the appraisal report lands on the table with a number lower than the contract price. That’s when this two-page form becomes the most important document in the deal.

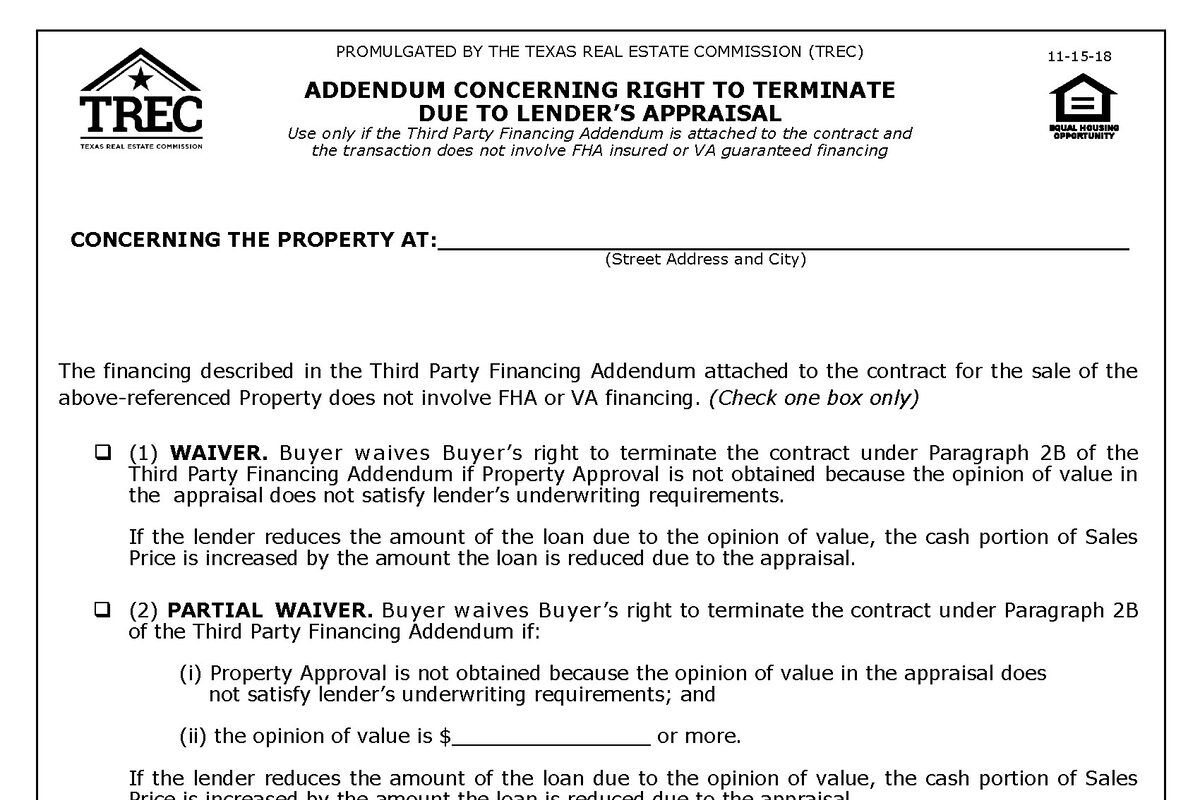

TREC 49-1 — the Addendum Concerning Right to Terminate Due to Lender’s Appraisal — gives the buyer the right to terminate the contract if the property doesn’t appraise at or above the sale price. It’s a standard addendum, but whether it’s included, excluded, or modified can change the trajectory of your entire transaction.

Table of Contents

▼How the Appraisal Addendum Works

When TREC 49-1 is attached to the contract, the buyer has a specific right: if the lender’s appraisal comes in below the sale price, the buyer can terminate the contract and get their earnest money back.

Without this addendum, the buyer doesn’t have an automatic exit based on the appraisal. They’re still on the hook for the contract price regardless of what the appraiser says. The financing might still fall apart if the lender won’t fund the gap, but the buyer’s termination rights are murkier without the addendum in place.

The addendum is simple in concept: it gives the buyer a clean out if the numbers don’t work. For sellers, it means the deal has one more contingency that could unwind it.

What Happens When the Appraisal Comes In Low

A low appraisal doesn’t automatically kill the deal. It starts a negotiation. Here are the typical paths forward:

The seller reduces the price to the appraised amount. This is the most common resolution. The seller takes less than they expected, but the deal closes. If the appraisal is only a few thousand below contract price, most sellers swallow it and move on rather than relist and start over.

The buyer pays the difference in cash. The lender will only lend based on the appraised amount. If the contract price is $350,000 and the appraisal comes in at $340,000, the buyer needs an extra $10,000 in cash above their planned down payment. Some buyers can do this. Many can’t.

They split the difference. The seller reduces the price by $5,000, the buyer brings an extra $5,000 to the table. Both sides give a little, and the deal closes.

Nobody budges and the buyer terminates. If the appraisal addendum is in the contract, the buyer walks, gets their earnest money back, and the seller relists. If the addendum isn’t in the contract, the buyer’s options are more limited — but the lender still won’t fund the shortfall, so the deal may collapse anyway.

Waiving the Appraisal Addendum

When a buyer submits an offer without TREC 49-1, they’re “waiving the appraisal.” This tells the seller: I’m buying this house at this price regardless of what the appraisal says.

From a seller’s perspective, this is a stronger offer. It removes one of the biggest contingencies in the contract. In a competitive market with multiple offers, a buyer who waives the appraisal is telling you they have the cash to cover any gap between the appraised amount and the contract price.

But here’s the practical reality: a buyer who waives the appraisal and then can’t cover a $15,000 gap doesn’t have the cash they implied they had. The deal still falls apart — it just gets messier. The buyer may try to renegotiate, or the lender kills the deal on the financing side. The appraisal addendum being absent doesn’t magically make the money appear.

When evaluating an offer with a waived appraisal, look at the whole picture. How much is the buyer putting down? Do they have proof of funds for the difference? A buyer putting 20% down who waives the appraisal is credible. A buyer putting 3% down who waives the appraisal may not have the reserves to back it up.

It’s also not all-or-nothing. The TREC 49-1 form has three options: a full waiver, a partial waiver with a floor value (buyer covers the gap as long as the appraisal is above a certain number), and an additional termination right that gives the buyer more protection. The partial waiver is a useful middle ground — the buyer takes on some appraisal risk without committing to cover an unlimited gap.

Strategy for Sellers

Price it right from the start. The best defense against a low appraisal is pricing based on recent comparable sales. If your contract price is supported by the comps, the appraisal will usually come in at or above the number.

Prepare a comp packet for the appraiser. When the appraiser comes to the property, have a one-page summary of the 3-5 most relevant comparable sales, plus a list of any improvements you’ve made with dates and costs. Appraisers aren’t required to use your comps, but a well-prepared packet can help if the comps they pull from MLS don’t tell the full story.

Know your bottom line before the appraisal comes back. Decide in advance how much you’re willing to reduce if the appraisal is low. Having a number in mind prevents emotional decision-making when the report arrives.

Weigh offers with appraisal waivers carefully. A waived appraisal addendum is attractive, but only if the buyer can actually back it up. Ask about proof of funds. A strong offer with the appraisal addendum attached can be better than a weak offer without it.

Understand the FHA/VA appraisal risk. FHA and VA appraisals have their own rules and the appraisal can stick with the property for months. This is covered by Paragraph 4 of the Third Party Financing Addendum, not by TREC 49-1. If your buyer pool includes FHA or VA buyers, read that article for the details.

The Honest Take

The appraisal addendum exists to protect the buyer from overpaying. For sellers, it’s one more contingency to manage. But a well-priced home in Houston rarely has appraisal problems — the comps support the price and the appraisal comes in fine.

Where it gets complicated is in a shifting market, with new construction competing against resale, or when a seller prices based on what they want rather than what the comps support. If your listing is priced based on solid comparable sales and presented well, the appraisal addendum is a formality. If it’s priced on hope, the addendum is the contract provision that brings you back to reality.

If you’re selling in Houston and want a broker who prices based on data — not optimism — get a free market analysis or start your listing.

Related Guides

- Third Party Financing Addendum in Texas

- Earnest Money vs Option Fee in Texas

- How to Handle Offers When Selling FSBO

- Discount Realtor Houston: Full-Service Listing for 1%

- Option Period in Texas Real Estate

- Release of Earnest Money in Texas

Selling a Home in Houston?

1% listing fee. Full service. No long-term contract.

Frequently Asked Questions

What is the appraisal addendum in Texas?

TREC 49-1, the Addendum Concerning Right to Terminate Due to Lender's Appraisal, gives the buyer the right to terminate the contract if the property appraises below the sale price. Without this addendum, the buyer doesn't have an automatic termination right based on appraisal alone.

Can the buyer terminate if the appraisal comes in low?

Only if the appraisal addendum (TREC 49-1) is part of the contract. If it is, the buyer can terminate and get their earnest money back if the appraisal is below the sale price. If the addendum isn't included, the buyer's options are more limited.

What does 'waiving the appraisal' mean in a Texas real estate offer?

It means the buyer is not including the appraisal addendum in their offer. They're telling the seller they'll proceed with the purchase regardless of what the appraisal says. This makes the offer stronger but shifts the risk to the buyer if the appraisal comes in low.

Does a low appraisal kill the deal?

Not necessarily. A low appraisal opens a negotiation. The seller can reduce the price, the buyer can pay the difference in cash, or they can split it. If the appraisal addendum is in the contract and no one budges, the buyer can terminate.

Does an FHA or VA appraisal stay with the property?

Yes. FHA appraisals are tied to the property for 180 days. VA appraisals are tied for 6 months. If the first buyer's FHA or VA appraisal comes in low, the next FHA or VA buyer will likely get the same number unless you can request a reconsideration or wait for the appraisal to expire.

{kind=link}