A Lender Document That Sellers Need to Understand

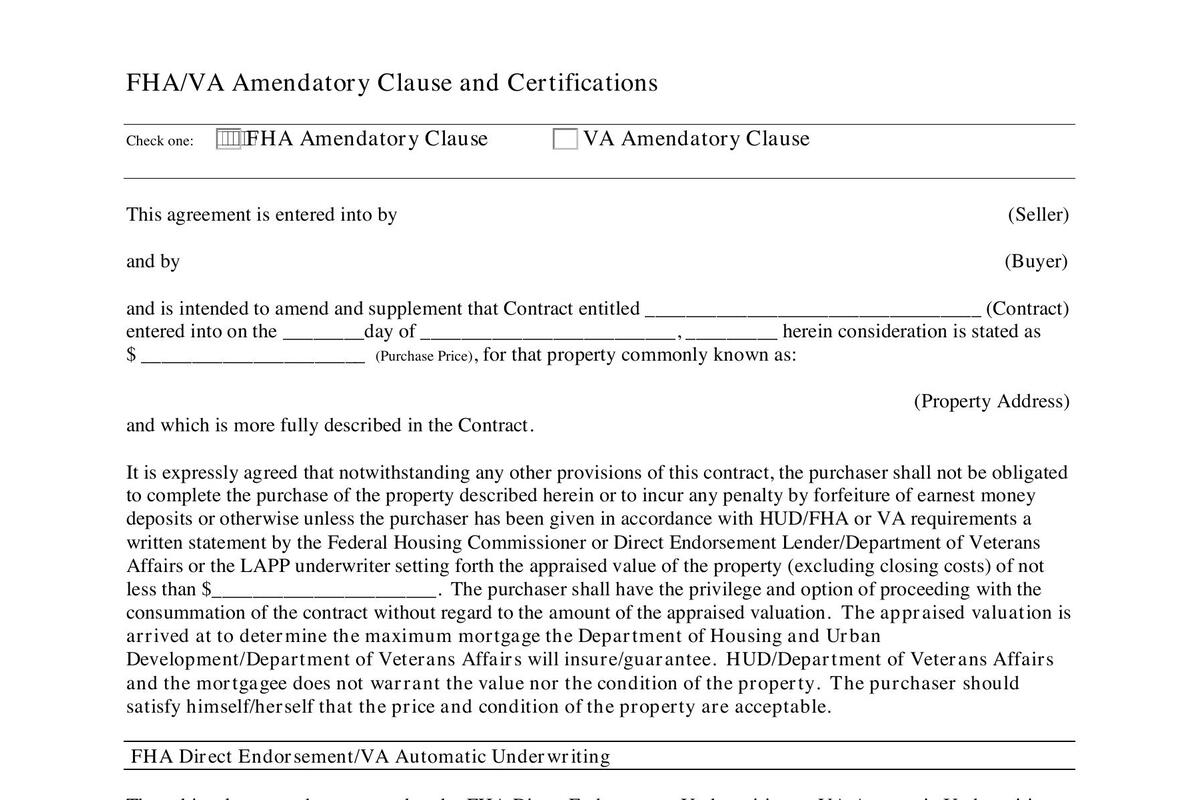

If your buyer is using FHA or VA financing, a document called the FHA/VA Amendatory Clause will show up in the paperwork. It’s not a TREC form. It’s not a TXR form. It comes from the buyer’s lender, and it’s required by HUD and the Department of Veterans Affairs on every FHA and VA transaction.

The core language is straightforward:

“The purchaser shall not be obligated to complete the purchase of the property described herein or to incur any penalty by forfeiture of earnest money deposits or otherwise, unless the purchaser has been given in accordance with HUD/FHA or VA requirements a written statement setting forth the appraised value of the property of not less than the contract price.”

In plain English: if the appraisal comes in below the sale price, the buyer can walk and get their earnest money back.

Table of Contents

▼How It Relates to the Texas Contract

If this sounds familiar, it should. Paragraph 4 of the Third Party Financing Addendum (TREC 40-11) already includes this exact protection for FHA and VA buyers. The TREC contract baked the amendatory clause language into the standard form.

So why does the lender send a separate document? Because HUD and the VA require a standalone signed acknowledgment from both buyer and seller — regardless of what the state contract says. It’s belt and suspenders. The protection exists in the contract and in the lender’s document.

What This Means for Sellers

You’re going to sign it. If the buyer has FHA or VA financing, this document is part of the deal. Don’t be surprised when it shows up — it’s standard.

The buyer can walk if the appraisal is low. Unlike the TREC 49-1 addendum on conventional loans where the buyer can waive or partially waive their appraisal termination right, the FHA/VA amendatory clause can’t be removed. The buyer always has the right to walk if the appraisal is below the contract price.

The buyer can still choose to proceed. The clause says the buyer “shall have the privilege and option of proceeding with consummation of the contract without regard to the amount of the appraised valuation.” If the buyer has the cash to cover the gap and wants the house, they can close. They’re just not forced to.

This is why FHA/VA offers carry more appraisal risk for sellers. On a conventional offer, the buyer can waive the appraisal addendum entirely — removing that contingency from the deal. On FHA/VA, the appraisal protection is always there. Combine that with the fact that FHA and VA appraisals stick with the property for a period of time, and you understand why some sellers weigh conventional offers more heavily.

Don’t Let It Scare You

Most FHA and VA transactions close without appraisal issues. If the property is priced based on solid comparable sales, the appraisal usually supports the price. The amendatory clause is a safety net for buyers — it doesn’t mean the deal is fragile.

FHA and VA buyers make up a significant portion of the Houston market. Refusing to consider government-loan offers because of the amendatory clause would shrink your buyer pool unnecessarily. The key is pricing correctly and understanding the appraisal risk going in.

Sell your home for just 1% commission.

Related Guides

Frequently Asked Questions

What is the FHA/VA amendatory clause?

A lender-required document that states the buyer is not obligated to complete the purchase if the appraised value comes in below the contract price. Both buyer and seller sign it. It protects the buyer from overpaying relative to the appraised value.

Is the amendatory clause a TREC or TXR form?

No. It's a lender-required document that comes from the buyer's mortgage company. In Texas, the same protection is already written into Paragraph 4 of the Third Party Financing Addendum (TREC 40-11), but the lender still requires a separate signed copy.

Can the buyer waive the amendatory clause?

The buyer can choose to proceed with the purchase even if the appraisal is low — that's their option. But the clause itself can't be removed from the transaction. It's required by HUD and the VA on every FHA and VA loan.

{kind=link}