When a Deal Falls Apart, the Money Doesn’t Just Disappear

Real estate contracts fall through. It happens more often than most people expect. When it does, the first question everyone asks is: who gets the earnest money?

The answer is never automatic. The title company holds the earnest money in escrow for the duration of the contract. They don’t pick sides, they don’t decide who’s right, and they don’t release funds because one party’s agent says so. Both the buyer and seller have to agree on where the money goes, and they document that agreement on the Release of Earnest Money form.

Table of Contents

▼What Is the Release of Earnest Money Form?

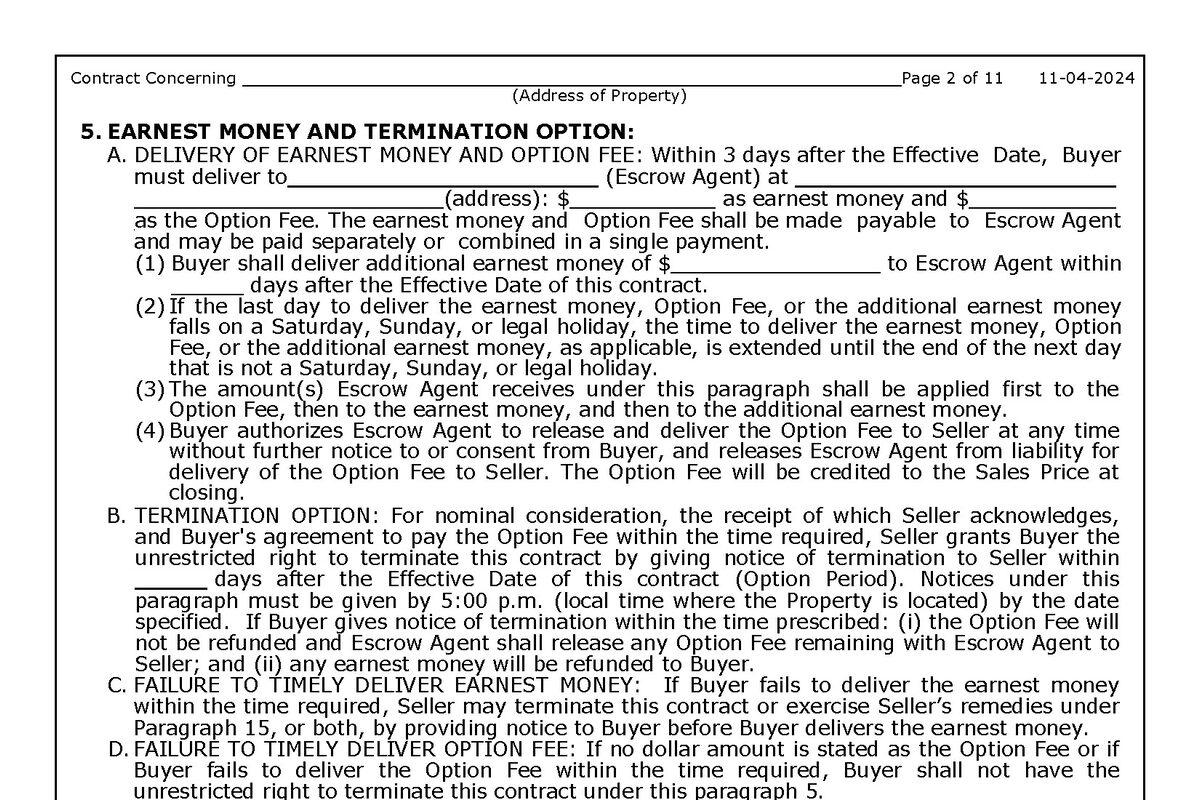

The Release of Earnest Money is TXR-1904 (formerly TAR-1904), a Texas REALTORS form — not a TREC form, though people call it that constantly.

The form is short, but don’t let that fool you. It does more than tell the title company where to send the deposit. Straight from the form: “This form provides for the release of the parties, brokers, and title companies from all liability under the contract (not just for disbursement of earnest money).” When you sign the TXR-1904, you’re releasing the buyer, the seller, both brokers, and the title company from all liability under the contract. That’s why you don’t sign it casually.

The form identifies the property, references the original contract, and specifies how the earnest money should be distributed — all to the buyer, all to the seller, or split. Both parties and both brokers sign it, it gets delivered to the title company, and the money moves.

Simple on paper. Not always simple in practice.

When Is This Form Used?

You’ll need a Release of Earnest Money any time a contract ends without closing. Here are the most common scenarios.

Buyer Terminates During the Option Period

This is the cleanest version. The buyer exercises their right to terminate during the option period, delivers written notice, and gets a full refund of the earnest money. The option fee is separate — the seller keeps that regardless.

Both parties sign the release, title processes the refund, everyone moves on. This is routine and rarely contested. The buyer paid for the right to walk away, and they used it.

Financing Falls Through

The buyer’s lender denies the loan or the appraisal comes in low enough that the lender won’t fund at the contract price. If the buyer followed the timeline in the Third Party Financing Addendum and provided proper documentation, they’re typically entitled to a full refund.

The buyer’s approval process is largely opaque to sellers — you’ll know whether financing was approved or not, but not the details of why. That’s just how it works. Most buyers are working in good faith toward closing, but as a seller it’s a reminder that a financed contract carries uncertainty all the way to the finish line.

Title Issues or Contingencies Not Met

The title search reveals a lien that can’t be cleared. The survey shows an encroachment. The buyer and seller can’t agree on inspection repairs. If a contract contingency fails and the contract allows termination under those circumstances, the earnest money typically goes back to the buyer.

Mutual Agreement to Cancel

Both parties decide it isn’t going to work and agree to walk away. No drama, no dispute. Everyone signs the release, the money goes back to the buyer (usually), and both sides move on.

Buyer Defaults After the Option Period

This is where it can get contentious. The option period has passed, the buyer has no contingency-based right to terminate, but they want out. Maybe they found another house. Maybe they got cold feet. Maybe their life situation changed.

The seller has a legitimate claim to the earnest money because the buyer is in default. The buyer disagrees and won’t sign the release. Now you have a standoff.

The release form doesn’t resolve disputes — it documents agreements. If the parties can’t agree, the money sits in escrow and the house stays off the market until everyone signs. Most sellers decide that getting back on the market is worth more than arguing over a few thousand dollars in earnest money. Some will stand on principle and take it to a lawsuit — which usually costs more in time and legal fees than the earnest money was worth in the first place.

What Happens If Both Parties Don’t Agree?

This is the question that brings most people to this article.

The title company cannot release earnest money without both signatures. Period. They’re a neutral third party holding funds in escrow. They don’t interpret the contract, they don’t decide who breached, and they don’t take sides.

If one party refuses to sign, here’s what happens:

The money sits. The title company holds it in escrow indefinitely. There’s no time limit. It can sit for months or years if nobody resolves the dispute.

Broker-to-broker negotiation. This is how most disputes get resolved. Your broker contacts the other side’s broker, they discuss the facts, and they find a compromise. Maybe they split the earnest money. Maybe one side realizes their position isn’t as strong as they thought. This is the fastest and cheapest path — and one of the reasons having a full-service broker matters.

Mediation. Most TREC contracts include a mediation clause. Before either party can file a lawsuit, they’re required to attempt mediation. A neutral mediator helps both sides reach an agreement. Costs are typically split. It’s not free, but it’s a fraction of what litigation costs.

Litigation. If mediation fails, either party can file a lawsuit. This is expensive, slow, and rarely worth it. Legal fees add up fast and often exceed the earnest money deposit itself. Most disputes that make it this far would have been better resolved at the broker or mediation stage.

Earnest Money vs Option Fee — Quick Reminder

People confuse these constantly.

Earnest money is a good-faith deposit held by the title company. Refundable under certain conditions. Typical amount in Houston: about 1% of the sale price.

Option fee is paid directly to the seller for the right to terminate during the option period. Non-refundable — the seller keeps it no matter what happens.

If the buyer terminates during the option period: the seller keeps the option fee, and the buyer gets the earnest money back. Two separate pots of money with different rules.

For the full breakdown, see earnest money vs option fee in Texas.

Practical Advice for Sellers

Know your rights before a deal falls apart. Understand the option period, the financing contingency, and what constitutes a valid termination. Don’t agree to release earnest money if the buyer didn’t follow the proper process.

Don’t refuse to sign out of spite. If the buyer terminated during the option period — where they have the unrestricted right to terminate for any reason — the earnest money goes back to them. Some sellers refuse to sign the release anyway, hoping to punish the buyer or squeeze something out of the situation. Imagine explaining that position in mediation or in front of a judge: the buyer exercised a contractual right you agreed to when you signed the contract, and you held up the process because you were angry about it. That’s not a position anyone wants to defend.

Don’t sign under pressure either. If the buyer’s agent is pushing you to sign the release immediately after a questionable termination, slow down. Talk to your broker. Understand whether the termination was valid before you agree to anything.

Get back on the market. A failed contract is a setback, not a dead end. The faster your broker gets the listing back to Active status in MLS, the less momentum you lose. Every day off-market is a day you’re not generating showing activity.

Keep copies of everything. Termination notices, emails, text messages, inspection reports, timeline documentation. If there’s a dispute, paperwork wins.

The Honest Take

A failed deal stings. You signed a contract thinking you were done — the showings, the open houses, the strangers walking through your home, the stress of keeping everything clean, the uncertainty. You were finally at the finish line. And then something happens a week before closing and the whole thing falls apart.

It’s natural to want to lash out. To look for someone to blame. To try to recover a month of mortgage payments, utilities, and holding costs by fighting over the earnest money deposit. When you were under contract, you and the buyer had a common goal — close the deal. Now that the sale is off, you have competing goals, and that shift can make tempers flare.

But take a step back and think about what you actually want. Your goal was never to win an earnest money dispute. Your goal was to sell your house. The fastest way to get back to that goal is to sign the release, get back on the market, and find the next buyer. Every week you spend in a standoff over $3,000-$5,000 is a week your house isn’t generating showings, and a week of holding costs you’re never getting back regardless of who wins the argument.

That doesn’t mean you roll over when a buyer is clearly in the wrong. But having a broker who has been through dozens of these — someone who can walk you through the situation and help you weigh your options — can be the difference between a resolved dispute and a six-month standoff that costs you more than the earnest money was ever worth.

One more thing, and we’ll be direct about this: we advocate hard for our sellers. That’s our job, and we don’t stop mid-transaction. Most of our clients are great to work with. But once the deal is resolved and the dust settles, if you’ve shown us that you’re someone who holds up legitimate releases out of spite, makes unreasonable demands, or drags the other side through fights you can’t win — we’ll fulfill our obligations and then we’ll part ways. Everyone has bad days, and we get it. This job is more than “sell home, get paid.” On any given day we’re a sounding board, a therapist, comic relief, a shoulder to cry on, a cheerleader, a project manager, a negotiator, and occasionally the person who talks you off the ledge at 10 PM on a Sunday. We’re here for all of that. But we’re here to help you sell your home — not to help you make someone else’s life miserable. The clients who do well with us are the ones who keep their eyes on the goal.

If you’re selling in Houston and want full-service representation at 1%, get a free market analysis or start your listing.

Related Guides

Selling a Home in Houston?

1% listing fee. Full service. No long-term contract.

Frequently Asked Questions

Who decides who gets the earnest money when a Texas contract falls through?

Both the buyer and seller have to agree. The title company holds the money in escrow and won't release it to either side without both signatures on the Release of Earnest Money form. If the parties can't agree, the money sits until they negotiate a resolution or a court orders the release.

How long does it take to get earnest money back in Texas?

Once both parties sign the Release of Earnest Money form and deliver it to the title company, the refund typically processes in 3-10 business days. The delay is almost always in getting both signatures, not in the title company's processing.

Does the buyer always get earnest money back if the deal falls through?

No. It depends on why the deal fell through and who caused it. If the buyer terminates during the option period or under a valid financing contingency, the buyer typically gets the money back. If the buyer defaults after the option period with no contractual right to terminate, the seller may be entitled to keep it.

What happens if the seller refuses to sign the Release of Earnest Money?

The title company holds the money in escrow indefinitely. The parties can negotiate, go to mediation (most TREC contracts require it before litigation), or ultimately file a lawsuit. In practice, most disputes get resolved through broker-to-broker negotiation.

Is the Release of Earnest Money form a TREC form?

No. The Release of Earnest Money is TXR-1904, a Texas REALTORS form (formerly TAR-1904). TREC promulgates the residential contract and certain addenda, but the release of earnest money form comes from the Texas REALTORS association.

{kind=link}