Three Ways to Handle a Low Appraisal — Before It Happens

The Third Party Financing Addendum already gives buyers the right to terminate if the property doesn’t satisfy the lender’s requirements — and a low appraisal is one of those requirements. TREC 49-1 / TXR 1948 modifies that right, giving the buyer and seller a way to negotiate the appraisal risk upfront.

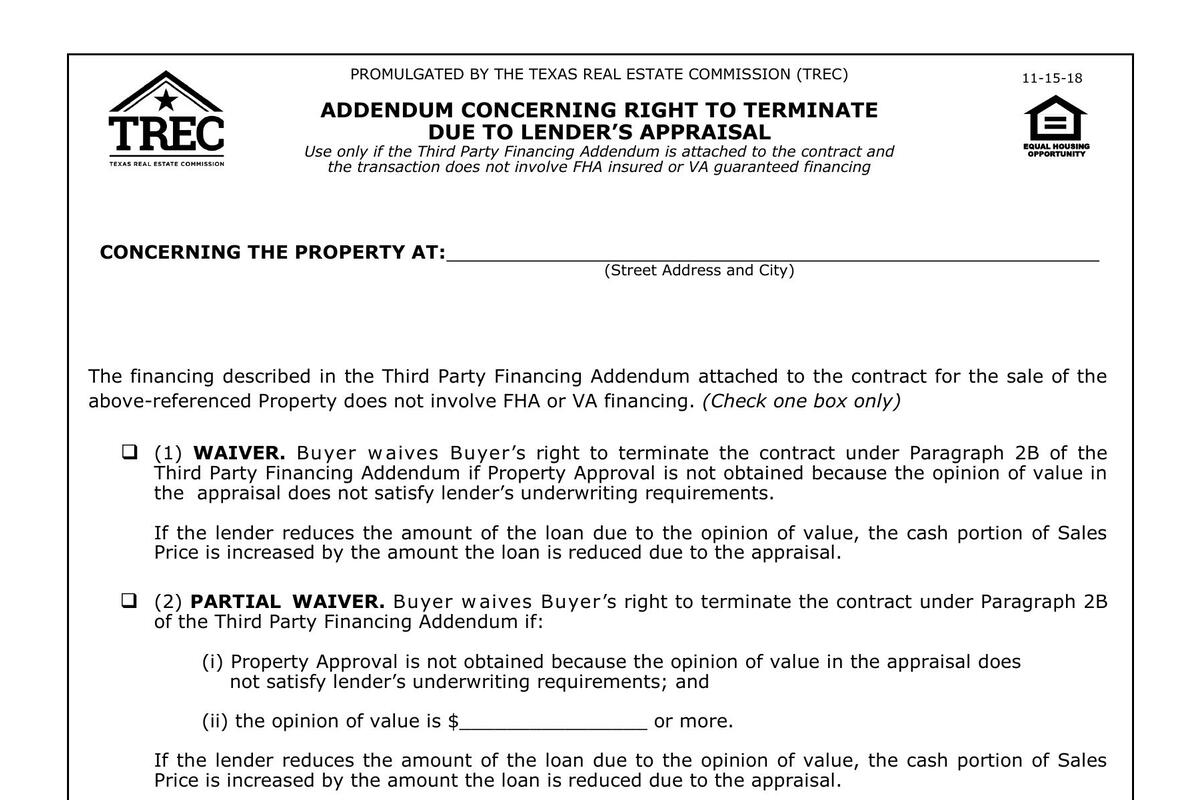

This addendum is only used on conventional financing — not FHA or VA, which have their own appraisal rules.

For a broader look at how appraisals affect your transaction, see our Appraisal Addendum guide.

Table of Contents

▼The Three Options

The form has three checkboxes. Only one gets checked.

Option 1: Full Waiver

The buyer waives their right to terminate if the appraisal comes in low. If the lender reduces the loan amount because the appraised value is below the sale price, the buyer covers the difference in cash. The sale price stays the same.

What this means for sellers: This is the strongest offer a buyer can make regarding appraisal risk. The buyer is telling you they’ll close regardless of what the appraisal says. In a competitive market, this can make a financed offer almost as strong as cash on the appraisal front.

What this means for buyers: You’re on the hook for the gap. If your appraisal comes in $20,000 low, you’re bringing an extra $20,000 to closing. Make sure you have the reserves before you check this box.

Option 2: Partial Waiver

The buyer waives their right to terminate — but only if the appraised value is at or above a specified dollar amount. Below that floor, the buyer retains the right to terminate.

Example: Sale price is $400,000. The partial waiver floor is set at $380,000. If the appraisal comes in at $385,000, the buyer covers the $15,000 gap. If it comes in at $375,000, the buyer can terminate.

What this means for sellers: You have some protection against a slightly low appraisal, but not a catastrophically low one. The floor number is negotiated — the closer it is to the sale price, the less protection the seller has.

Option 3: Additional Right to Terminate

This one goes the other direction. Instead of waiving rights, the buyer gets an additional termination right beyond what the financing addendum already provides. The buyer can terminate within a specified number of days if the appraised value is below a specified dollar amount, and must deliver a copy of the appraisal to the seller.

What this means for sellers: The buyer is adding more protection for themselves, not less. This gives them a faster, cleaner exit if the appraisal is below their comfort level. You’d typically only agree to this if the buyer is giving you something else in return — a higher price, fewer contingencies elsewhere, or a larger earnest money deposit.

When This Addendum Comes Up

This addendum shows up in two situations:

Competitive markets. Buyers waive or partially waive appraisal termination rights to make their offer more attractive. A full waiver tells the seller the deal will close regardless of the appraisal — powerful when competing against multiple offers.

Overpriced markets or unusual properties. When there’s a real risk the appraisal won’t support the price — limited comps, unique features, rapidly appreciating area — the buyer or their agent may push for Option 3 to add extra protection.

What Sellers Should Know

A full waiver doesn’t guarantee the buyer has the cash. The buyer can check Option 1, but if the appraisal comes in $30,000 low and they don’t have $30,000, the deal still falls apart — just for a different reason (financing denial). Ask your broker about the buyer’s financial strength before putting too much weight on the waiver.

The partial waiver floor is negotiable. Push for a floor that’s close to realistic market value. A floor set $50,000 below the sale price isn’t meaningful protection.

This form only covers appraisal value. The financing addendum covers other property approval issues (condition, insurability, etc.). This addendum only modifies the appraisal piece.

Sell your home for just 1% commission.

Related Guides

Frequently Asked Questions

What is the Right to Terminate Due to Lender's Appraisal addendum?

TREC 49-1 (TXR 1948) modifies the buyer's rights when the appraisal comes in low. It gives three options: the buyer waives the right to terminate over a low appraisal, partially waives it above a floor value, or gets an additional termination right below a specified value.

Does this addendum apply to FHA or VA loans?

No. The form explicitly states it's only for transactions that do not involve FHA insured or VA guaranteed financing. FHA and VA loans have their own appraisal protections.

What happens if the buyer waives the appraisal termination right?

If the buyer checks the full waiver (Option 1), they can't terminate because of a low appraisal. If the lender reduces the loan amount, the buyer must cover the difference in cash. The sale price doesn't change.

{kind=link}