Staying in Your Home After You Sell It

You’ve closed on your house. The money is in your account. But you’re not ready to move out yet. Maybe your next home closes in a few days and the timing didn’t quite line up. Maybe you need a week to finish moving. Maybe you’re buying another property and the closings are a few days apart — things rarely line up perfectly.

A seller’s temporary residential lease — commonly called a leaseback — lets you stay in the property after closing. The buyer owns the home, but you remain as a tenant for a defined period, paying rent and following the terms of the lease.

It’s one of the most common arrangements in residential real estate, and it solves a real logistical problem. But the terms matter, and sellers who treat it as an afterthought can end up with a bad deal.

Table of Contents

▼How a Seller’s Leaseback Works

The leaseback is negotiated as part of the original purchase contract. You don’t wait until closing to bring it up — it’s discussed during the offer stage and attached to the contract as an addendum.

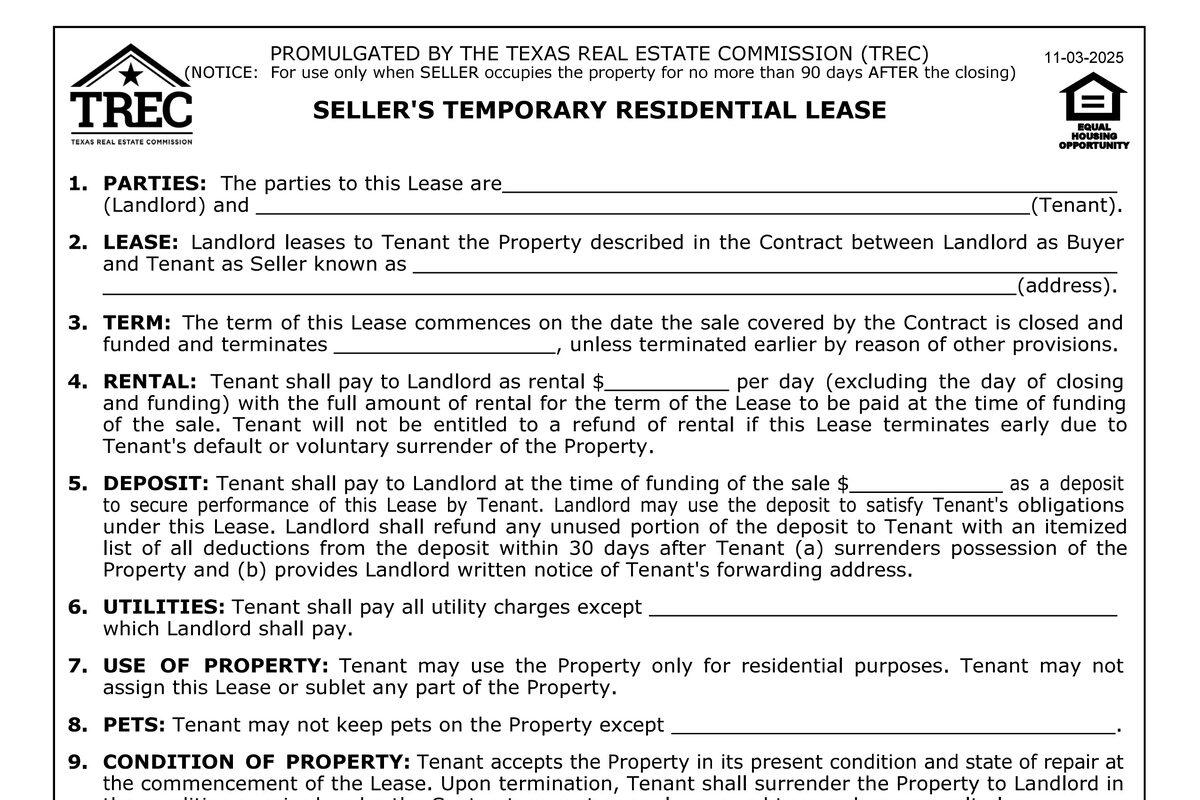

Two forms are commonly used in Texas:

- TREC 15-7 — the Texas Real Estate Commission’s Seller’s Temporary Residential Lease form

- TXR 1910 — the Texas REALTORS version (formerly TAR)

Both accomplish the same thing. The form covers the lease term, daily rental rate, security deposit, maintenance obligations, and what happens if the seller doesn’t vacate on time.

Here’s the basic structure: the sale closes normally. The buyer gets the deed. The seller’s proceeds are disbursed. Then the seller stays in the property as a tenant under the leaseback terms. When the lease term ends, the seller moves out, the buyer gets the security deposit back (minus any deductions for damage or unpaid rent), and the buyer takes possession.

Key Terms in the Lease

Lease Term

The TREC form limits the leaseback to 90 days. In practice, most leasebacks are a few days to a couple of weeks — it’s usually a courtesy stay to allow the seller to finish moving or to align timing on their next property. We rarely see leasebacks much past two to three weeks.

If you know you’ll need a leaseback, you have options. You can put the requirement in the listing agent remarks so buyer’s agents — at least the ones who read — can advise their buyers upfront. Or you can negotiate a longer closing date instead, which avoids the leaseback entirely and keeps things simpler for everyone.

Some buyer’s lenders restrict leaseback terms — certain loan programs won’t allow more than 60 days, and some conventional lenders get uncomfortable past 30. If you need more than 90 days, the arrangement moves beyond a temporary residential lease and into standard landlord-tenant territory. Different rules, different forms, different legal exposure.

Daily Rental Rate

The most common formula is the buyer’s daily PITI — their monthly principal, interest, taxes, and insurance divided by 30. This covers the buyer’s carrying cost while you occupy their property.

On a $350,000 home with a conventional loan, the daily PITI might be $75-100/day depending on the rate, taxes, and insurance. Over 30 days, that’s $2,250-3,000 in rent.

Some buyers charge a premium above PITI — especially in a seller’s market where the buyer has leverage. Some leasebacks are negotiated at zero rent as a concession to get the deal done. The rate is negotiable, and everything depends on the strength of the market and the dynamics of the specific deal.

Security Deposit

The lease requires a security deposit held by the title company or the buyer’s agent. This protects the buyer against damage to the property or the seller overstaying the lease.

Typical security deposit amounts in Houston range from one month’s rent equivalent to the full lease amount. Some buyers ask for more if the leaseback term is longer. The deposit is refundable — minus deductions for damage beyond normal wear and tear, unpaid rent, or cleaning costs if the seller leaves the property in poor condition.

Maintenance and Utilities

During the leaseback, the seller is responsible for maintaining the property in its current condition. That means keeping the lawn mowed, the pool maintained (if applicable), the HVAC running, and the property clean. You’re a tenant now — treat it like someone else’s property, because it is.

Utilities stay in the seller’s name during the leaseback. Don’t transfer them to the buyer until you move out. If the utilities get switched and the power goes off while you’re still living there, that’s a mess nobody wants to deal with.

Insurance

This is the part most people overlook. Once the sale closes, the seller’s homeowner’s insurance policy is canceled or no longer covers the property — the buyer has their own policy now. But the buyer’s policy may not cover the seller’s personal belongings or liability while the seller is living there.

The lease forms address this. The seller should maintain renter’s insurance during the leaseback period to cover personal property and personal liability. It’s inexpensive — usually $15-30/month — and it closes the gap between the buyer’s homeowner’s policy and the seller’s exposure.

Holdover Penalties

If the seller doesn’t move out by the end of the lease term, the daily rental rate typically increases — often 1.5 to 2 times the original rate. This is spelled out in the lease. If the seller still won’t leave after the holdover period, the buyer may need to pursue formal eviction through the courts.

Don’t let it get there. If you know you’re going to need more time, communicate with the buyer before the lease expires and negotiate an extension. Surprising the buyer on move-out day is the fastest way to turn an amicable transaction into a hostile one.

How It Differs from a Buyer’s Temporary Lease

A buyer’s temporary residential lease is the reverse — the buyer moves in before closing. We advise against those in every situation.

A seller’s leaseback has its own risks for the buyer that people don’t talk about. The seller got paid, they’re still in the home, and if they didn’t want to sell in the first place — maybe they were forced to for financial reasons — they now have a pile of cash and zero incentive to leave. The holdover penalties and security deposit are supposed to motivate a timely exit, but for a seller who’s comfortable and in no rush, those amounts may not matter.

This is one of the reasons a final walkthrough exists. Most people think the final walkthrough is just about checking property condition — and it is — but one of those conditions is confirming the seller has actually moved out. If you can avoid a leaseback by adjusting the closing date, that’s almost always the better move. The buyer does their walkthrough, confirms the property is vacant and in the expected condition, and closes.

Strategy and Practical Advice

Negotiate the leaseback during the offer stage. Don’t wait until closing week to ask if you can stay. Build it into the contract from the beginning so the buyer knows the full picture before they commit.

Keep the term as short as you realistically need. Asking for 60 days when you only need 30 creates unnecessary friction. Shorter leasebacks are easier for buyers to accept and less likely to trigger lender objections.

Budget for the rent. If you’re paying $100/day for 45 days, that’s $4,500 coming out of your proceeds. Factor it into your net calculations from the start so there are no surprises at closing.

Maintain the property. You’re living in someone else’s house. Treat it accordingly. Any damage beyond normal wear and tear comes out of your security deposit — or worse, leads to a dispute that costs more than the damage itself.

Get renter’s insurance. It’s cheap and it covers the gap. If a pipe bursts during your leaseback and damages your furniture, the buyer’s homeowner’s policy covers the structure — not your belongings. Renter’s insurance solves this.

Have your move-out plan locked down before closing. Know your move-out date, have movers booked, and have your next living situation confirmed. The leaseback is a bridge, not a long-term plan. The cleaner your exit, the smoother the security deposit refund.

Don’t overstay. The holdover penalties are real, and the buyer’s patience is finite. Move out on time. Leave the property clean. Return all keys, garage remotes, and gate codes. End the transaction the same way you started it — professionally.

The Honest Take

A seller’s leaseback is one of the most practical tools in Texas real estate. It gives you breathing room between selling your current home and getting into your next one. The terms are straightforward, the risk is manageable, and it solves a timing problem that trips up thousands of sellers every year.

Just don’t treat it as an afterthought. The rental rate, the term, the security deposit, and the insurance all need to be addressed upfront. Negotiate the leaseback with the same attention you give the sale price — because it’s part of the same deal.

If you’re selling in Houston and need a broker who can negotiate a leaseback that works for your timeline, get a free market analysis or start your listing.

Related Guides

Selling a Home in Houston?

1% listing fee. Full service. No long-term contract.

Frequently Asked Questions

What is a seller's temporary residential lease in Texas?

It's a leaseback that lets the seller stay in the property after closing for a short period — typically a few days to a couple of weeks. The buyer owns the home but the seller remains as a tenant, paying a daily rental rate until they move out.

How long can a seller stay after closing in Texas?

The TREC form (15-7) limits the leaseback to 90 days. In practice, most leasebacks are a few days to a couple of weeks — just enough time to finish moving or align timing on the seller's next property. Lenders sometimes impose their own limits as well.

How much rent does the seller pay during a leaseback?

The most common formula is the buyer's daily PITI — principal, interest, taxes, and insurance divided by 30. This covers the buyer's cost of owning the property while the seller occupies it. The rate is negotiable, and some buyers charge a premium above PITI.

What happens if the seller doesn't move out on time?

The lease typically includes a daily holdover penalty — often 1.5 to 2 times the daily rental rate. If the seller still won't leave, the buyer may need to pursue eviction through the courts. The security deposit is also at risk.

Is a seller's leaseback risky for the buyer?

Less risky than a buyer's temporary lease because the seller has already been paid — they received their sale proceeds at closing and have no financial leverage over the buyer. The main risk to the buyer is the seller damaging the property or overstaying the lease term.

{kind=link}