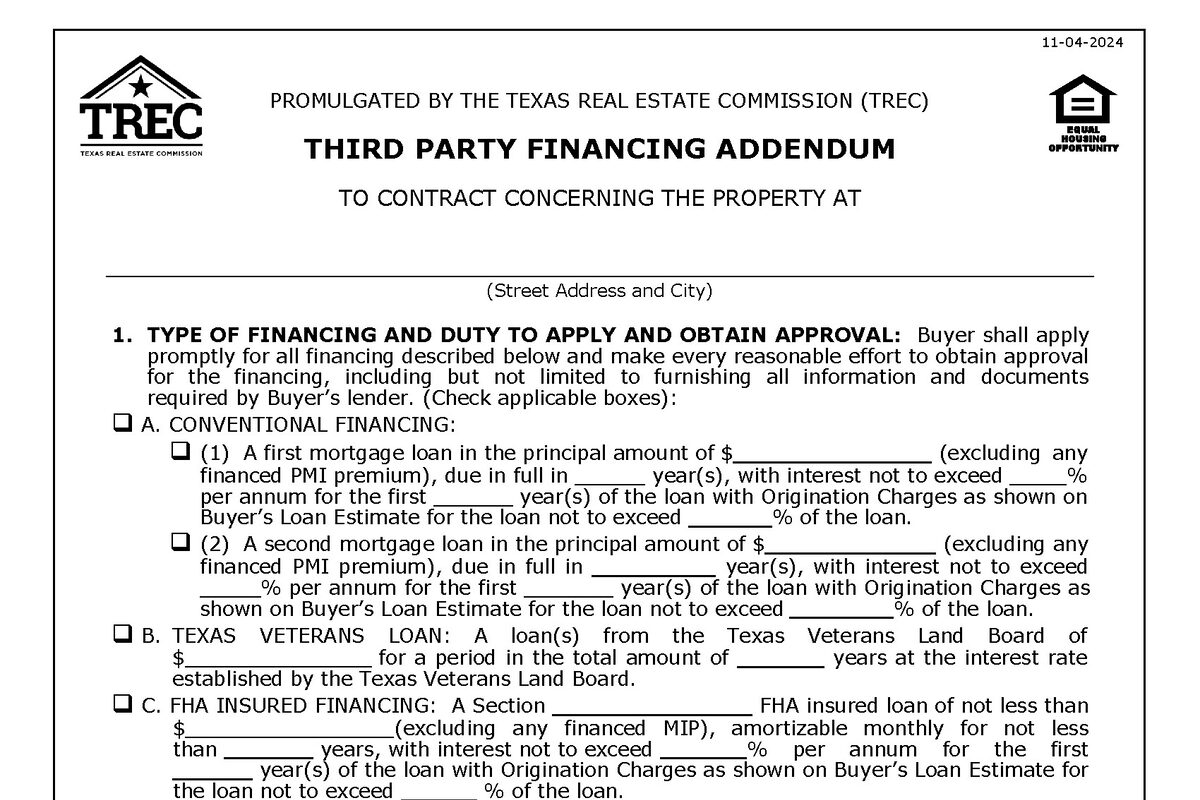

Every Financed Offer Comes With This Addendum

If a buyer is getting a mortgage to buy your house — and roughly 80% of buyers are — there’s a Third-Party Financing Addendum stapled to the contract. It’s TREC form 40-11, and it’s one of the most consequential documents in the entire deal.

This addendum tells you what kind of loan the buyer is getting, how much they’re borrowing, and the deadline by which they need lender approval. For sellers, it represents the single biggest risk in a financed transaction: the buyer’s ability to actually close.

Table of Contents

▼What TREC 40-11 Actually Covers

The addendum has several blanks that matter. Each one affects your risk as a seller.

Loan type. Conventional, FHA, VA, or USDA. Each type comes with different requirements for the property — not just the buyer. More on that below.

Loan amount. The dollar amount the buyer is borrowing. Combined with their down payment, this should equal the sales price. If the math doesn’t add up, ask questions before you sign.

Interest rate. The maximum interest rate the buyer will accept. If rates move above this number before closing and the buyer can’t lock a rate at or below it, that’s grounds to terminate under the addendum. In a rising rate environment, this blank matters more than sellers realize.

Origination charges. The maximum loan fees the buyer will pay, expressed as a percentage of the loan amount. If the lender’s fees exceed this number, the buyer has another exit path.

Financing approval deadline. This is the date that matters most. It’s the deadline by which the buyer must obtain financing approval from their lender. If they can’t get it done by this date, either party can terminate the contract.

The Financing Approval Deadline

This is the blank you should care about more than any other.

Financing deadlines typically fall 21-30 days from the contract execution date, but the timeline is largely lender-dependent. Good lenders usually fall inside that range. In a hot market where lenders are busy, it’s not unusual to see 45-day contracts where the extra time was requested by the lender themselves.

Regardless of the timeline, stay on top of the lender. Every document request from a lender seems to arrive at precisely 5:00 PM when their phone system rolls to voicemail. As a buyer, get that document back to them before they open tomorrow — don’t let it sit in your inbox. As a seller, you or your broker should be getting regular updates from the lender. A lender who goes dark and stops responding is a bad signal for how a deal is going. Everyone worries about title, but it’s the lenders that tank deals. They told their buyer they could get them financed — but that wasn’t always true.

Here’s what happens at the deadline:

Buyer gets approved before the deadline. Great. The deal moves toward closing. One less thing to worry about.

Buyer doesn’t get approved and terminates. They provide notice that financing was not obtained, terminate under the addendum, and get their earnest money back. You’re back on the market. It stings, but at least you know where you stand.

Buyer doesn’t get approved and doesn’t terminate. This is the one that catches people off guard. If the deadline passes and the buyer does nothing — doesn’t terminate, doesn’t provide approval — they’ve waived the financing contingency. Their earnest money is now at risk. But that doesn’t mean the seller suddenly has an easy exit. The contract is buyer-centric — sellers have very few outs. If you’re in this situation, talk to your broker about your options.

The key takeaway: the financing deadline is a use-it-or-lose-it protection. If the buyer doesn’t exercise their right to terminate by the deadline, the right goes away.

Financing Approval vs Clear to Close

These are two different things, and confusing them will cost you time.

Financing approval means the lender has reviewed the buyer’s credit, income, assets, and employment — and has reviewed the property through the appraisal — and approved the loan. This is what the addendum deadline refers to.

Clear to close comes later. It means underwriting has signed off on every last condition, the loan documents are being prepared, the lender is ready to fund, and title has closing instructions. This typically happens days — sometimes hours — before closing.

A buyer can have financing approval on day 25 and not be clear to close until day 42. That gap is normal. Frustrating, but normal. Lenders are harder to get on the phone than a friend of a friend you loaned money to. Once they have the approval, they move at their own pace getting to clear to close. Your broker’s job is to stay on top of them — and trust me, it takes effort.

Credit Approval vs Property Approval

Here’s a distinction most sellers don’t think about until it bites them.

The lender approves two things separately: the buyer and the property. The buyer can have perfect credit, solid income, and plenty of cash reserves — and the loan can still fail because of the property.

The appraisal is part of financing. The lender orders an appraisal to confirm the property’s value supports the loan amount. If the appraisal comes in below the contract price, the lender won’t approve the full loan. Now you’re negotiating — the buyer brings cash to cover the gap, you reduce the price, or you meet in the middle. A low appraisal at day 25 can blow up a deal that looked rock-solid. If you’re dealing with appraisal concerns, the Appraisal Addendum is worth understanding too.

Property condition matters too. Depending on the loan type, the appraiser may flag condition issues that the lender requires to be fixed before closing.

FHA and VA Loans: Extra Property Requirements

Not all loan types are created equal from the seller’s perspective.

FHA loans require the property to meet HUD’s Minimum Property Requirements. The appraiser isn’t just checking value — they’re checking for health and safety issues. If the appraiser flags something, the lender requires it to be repaired before closing. That means you’re paying for lender-required repairs that a conventional loan might never have flagged.

VA loans have similar property requirements. The appraiser checks for the same types of issues, and the lender won’t fund until they’re resolved.

Both FHA and VA appraisals “stick” with the property for a period of time — meaning if the deal falls apart and your next buyer is also FHA or VA, they may be stuck with the same appraised value. You can challenge an appraisal through a Reconsideration of Value (ROV) or request a correction if there are objective errors, but these rarely result in a change unless you have solid comparable sales the appraiser missed. This usually isn’t an issue, but if your home is priced aggressively and your buyer pool is mostly FHA or VA buyers, a low appraisal on the first deal can follow you into the next one.

This is why some sellers hesitate on FHA and VA offers. It’s not discrimination — it’s risk management. An FHA offer at $400,000 with potential lender-required repairs and a strict appraisal is a different deal than a conventional offer at $400,000 with fewer strings attached.

Why Sellers Should Care About This Addendum

The financing addendum is the biggest risk factor in any financed deal. Here’s why:

It gives the buyer a contractual exit. If financing falls through, the buyer terminates and walks away with their earnest money. You’ve had your house off the market for 3-4 weeks with nothing to show for it.

The timeline is long. A 30-day financing deadline means you’re waiting a month to find out whether the buyer can actually close. Meanwhile, other buyers have moved on to other homes.

You’re depending on a third party you have no control over. The lender. You can’t call them, you can’t speed them up, and you can’t make them do their job. Your broker can push, but some lenders are just slow. A bad lender can drag an otherwise solid deal right up to the deadline and then deny the loan at the last minute.

This is exactly why cash offers are so attractive to sellers. No financing addendum, no lender, no appraisal requirement, no 30-day uncertainty. Cash deals close in 14-21 days and the only real contingency is the option period.

One thing to watch for: buyers who offer cash to get their offer accepted and then try to substitute financing after the contract is executed. If the contract says cash, it means cash. If the buyer wants to finance the purchase, that’s a different deal than the one you agreed to. They’re free to refinance after closing, but the terms of the contract are what you accepted. Your broker should be watching for this. If you’re weighing offers and want to understand the full picture, how to handle offers breaks down what to look at beyond price.

Strategy: Shorter Deadlines Favor Sellers

If you’re in a strong market position — multiple offers, desirable property, good location — you can negotiate a shorter financing deadline. Instead of 30 days, push for 21. A well-prepared buyer with a competent lender can hit that timeline. A buyer who’s barely pre-qualified with an online lender probably can’t.

A shorter deadline does two things: it reduces the amount of time your house sits in limbo, and it filters for stronger buyers. If a buyer pushes back hard on a 21-day financing deadline, that tells you something about the strength of their financing.

Your broker should be advising you on this during offer negotiations. It’s one of several levers you have beyond just the sales price.

Pre-Approval Letters: Not All Are Equal

When a financed offer lands on your table, it comes with a pre-approval letter. Look at it carefully.

Pre-qualification means the buyer told the lender some numbers and the lender gave a rough estimate. No documents verified. This is essentially a guess.

Pre-approval means the lender actually reviewed pay stubs, tax returns, bank statements, and credit reports. This is substantially more reliable — but agents sometimes joke that a pre-approval letter isn’t worth the paper it’s printed on, and there’s some truth to that. The buyer still has to clear underwriting, and underwriting looks at both the buyer and the property.

Full underwriting upfront is the strongest position a buyer can be in. When a house is being purchased, both the buyer and the property go through underwriting. A buyer can complete their side of underwriting before they even make an offer — credit, income, assets, employment, all verified and approved. The only remaining step is the property side (appraisal and title). A buyer who tells the listing agent they’ve already been through underwriting is sending a powerful signal, especially in a competitive market. It can shorten the time under contract significantly and make a financed offer almost as clean as cash.

If the letter says “pre-qualified” instead of “pre-approved,” the financing is weaker than it looks. A strong pre-approval from a reputable local lender paired with realistic terms on the financing addendum — that’s an offer worth taking seriously. A buyer who’s already been through underwriting is even better.

When the Lender Asks for More Time

It happens. The financing deadline is approaching and the buyer’s agent calls asking for an extension. The lender needs a few more days.

You’re not obligated to grant it. And we don’t believe in free lunches.

An extension costs the seller real money. Mortgage, utilities, lawn and pool maintenance, insurance, taxes, HOA — those bills don’t stop because the buyer’s lender is slow. We ask our sellers to calculate their daily holding cost. $100 a day? $150? That’s $700-$1,050 for a one-week extension. Late in a transaction the seller has often already moved out, so they’re carrying the house on top of wherever they’re living now.

If we grant an extension, the buyer needs to give something to get something. Sometimes that’s a price increase to cover the holding costs — but if the appraisal was tight or the lender’s underwriting is already stretched, adding to the sale price creates problems. So instead we look at other places on the contract: reduce a repair credit the seller already agreed to, shift the cost of the owner’s title policy to the buyer, remove the home warranty, split costs that were previously one-sided. There are places you can recover a thousand dollars on a contract without touching the sale price.

Decline the extension if you’ve lost confidence in the buyer’s ability to close, if delays have been a pattern throughout the transaction, or if you have backup offers ready. If you’re managing the contract-to-close process yourself, this is one of the harder judgment calls you’ll face.

Your broker should be having a direct conversation with the buyer’s agent to find out what’s actually going on before you make this decision.

Related Guides

Selling a Home in Houston?

1% listing fee. Full service. No long-term contract.

Frequently Asked Questions

What is the Third-Party Financing Addendum in Texas?

TREC 40-11 is a standard addendum attached to any Texas residential contract where the buyer is getting a mortgage. It spells out the loan type, loan amount, interest rate cap, origination charges, and the deadline by which the buyer must get financing approval.

What happens if the buyer can't get financing by the deadline?

The buyer can terminate the contract and receive a full refund of their earnest money. If the deadline passes and the buyer does not terminate, they waive the financing contingency and their earnest money is at risk.

Does a cash offer use the Third-Party Financing Addendum?

No. Cash buyers don't need lender approval, so the addendum isn't attached to the contract. This eliminates financing risk entirely — one of the main reasons sellers prefer cash offers.

What is the difference between financing approval and clear to close?

Financing approval means the lender has approved the buyer's loan based on creditworthiness and the property meeting lender requirements. Clear to close comes later — it means underwriting is fully complete and the loan is ready to fund. They are two different milestones.

Can a seller refuse to extend the financing deadline?

Yes. The seller is under no obligation to grant an extension. Whether to extend depends on the circumstances — is the lender just slow, or is the buyer struggling to qualify? Talk to your broker about your options.

{kind=link}